Introduction

Fintech marketing is harder than it looks from the outside.

You're operating in a regulated industry where trust takes years to build and seconds to lose. Your product is often complex, your audience is often sceptical, and the competitive set changes faster than most marketing plans can keep up with. Whether you're selling direct to consumers or to enterprise buyers, the margin for vague, unfocused marketing is thin.

A fintech marketing strategy is the set of decisions that determine how you allocate time, budget, and people to achieve a specific commercial outcome. It's not a channel plan. It's not a content calendar. It's the thinking that sits underneath those things and makes them coherent.

Global fintech revenues reached approximately $650 billion in 2025, growing at around 21% year on year, according to McKinsey's "The Next Age of Fintech" report. The sector is projected to reach $1.5 trillion by 2030. The opportunity is real, but so is the competition for attention, trust, and market share across every segment of it.

This guide, updated for 2026, walks through the framework we use at Curious Cat Digital when building strategies for fintech clients, from consumer-facing neobanks and payment apps to B2B RegTech and financial data platforms.

Contents

The fintech industry

What is a fintech marketing strategy?

Why fintech marketing strategies fail

The 5 pillars of a fintech marketing strategy

Fintech branding

The fintech customer journey

Executing your fintech marketing strategy

Fintech inbound marketing

Fintech demand generation

ABM in fintech

Fintech product marketing tactics

Fintech content marketing

Developing your fintech marketing plan

Working with a fintech marketing agency

The fintech industry

Fintech has become a fundamental layer of how financial services operates globally.

The numbers reflect that. Global fintech revenues reached approximately $650 billion in 2025 and are projected to reach $1.5 trillion by 2030, according to BCG and QED Investors. That represents a roughly sixfold increase from 2021. And yet, for all the growth, fintechs currently capture only around 4% of total global financial services revenues, per McKinsey. The headroom is significant. So is the competition for it.

The UK sits at the centre of this. With over 3,300 fintech firms, a $10.96 billion investment market in 2025, and the largest fintech industry in Europe by most measures, KPMG's Pulse of Fintech consistently places London among the world's top two fintech hubs alongside New York.

What makes fintech marketing different

A few things separate fintech from other sectors when it comes to marketing.

Regulation shapes everything. What you can claim, how you can communicate, and how long it takes for a buyer to say yes are all affected by the regulatory environment. The EU's Digital Operational Resilience Act, which came into full application in January 2025, has added a new layer of vendor scrutiny for B2B fintech. FCA Consumer Duty obligations shape what consumer-facing fintechs can promise and how they must support customers after acquisition. Marketing that ignores these constraints creates commercial and legal risk.

Trust is the product. Financial services is an industry where trust is the primary purchase criterion. Edelman's 2025 Trust Barometer shows global financial services trust at 64%, the first time the sector has crossed into "trusted" territory since 2008. That trust is fragile. Marketing that overpromises, or is vague about what a product actually does, erodes it quickly and durably.

The buying process is longer and more complex than most. Whether you're acquiring consumers through a crowded app store or selling compliance infrastructure to a regulated bank, decisions aren't made quickly or by one person. A fintech marketing strategy has to work across that full length and complexity, not just at the moment of intent.

What is a fintech marketing strategy?

A strategy answers questions a channel plan never gets around to asking.

Who exactly are we trying to reach, and why would they choose us over every available alternative, including doing nothing? What do they believe before they encounter us, and what do we need them to believe afterwards? What does success look like in 90 days, in 12 months, in three years, and how does marketing connect to those numbers?

The answers look different depending on your model. A consumer fintech might be competing for attention in a crowded app store, trying to convert free users to paid, or rebuilding trust after a press cycle that didn't go well. A B2B fintech might be trying to get onto shortlists at financial institutions before procurement processes begin. The strategic questions are the same. The answers diverge significantly.

What stays constant across both: a fintech marketing strategy needs to start from a commercial outcome and work backwards, not start from a set of channels and hope for the best.

Why fintech marketing strategies fail

There are patterns to this. We see the same ones regularly enough that they're worth naming.

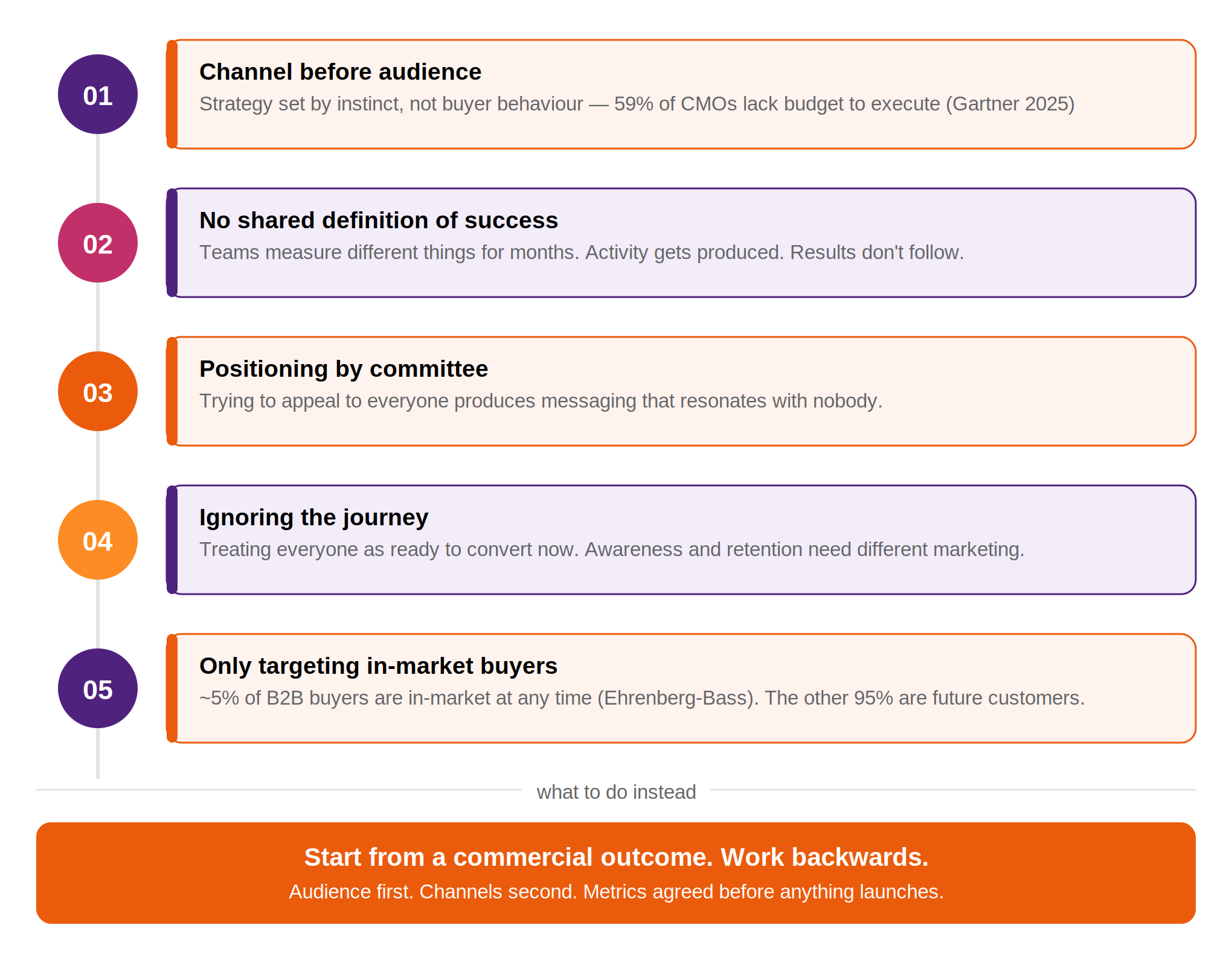

Channel selection before audience definition. A competitor is winning on TikTok or LinkedIn. Suddenly that's the strategy. Or a new CMO arrives with a background in paid search and the whole budget swings that way. Channel selection driven by instinct rather than audience behaviour is one of the most common and most expensive mistakes in fintech marketing. Gartner's 2025 CMO Spend Survey found that 59% of CMOs say they have insufficient budget to execute their strategy, which makes getting channel prioritisation right from the start rather important.

No shared definition of success. Ask ten fintech marketing teams what a lead is and you'll get ten different answers. Or ask what counts as an activation event for a consumer product, and find that marketing, product, and commercial teams have been measuring different things for months. Without agreement on what success looks like, you produce activity and measure it selectively.

Positioning by committee. Fintech markets are crowded. The temptation is to be relevant to everyone, which produces messaging that resonates with nobody. Strong positioning requires the courage to be specific, to say clearly who you are for and, implicitly, who you are not for. This applies equally to a consumer-facing payments app and to a B2B compliance platform.

Ignoring the journey. Customers and buyers go through stages before they make a decision, whether they're a consumer downloading a new banking app or a procurement team at a mid-market bank. Marketing that treats everyone as ready to convert right now will consistently underperform against marketing that meets people where they actually are.

Only targeting people who are actively looking. The Ehrenberg-Bass Institute's 95-5 Rule, validated by the LinkedIn B2B Institute, finds that only around 5% of buyers are in-market at any given time in B2B. Consumer fintech faces an analogous challenge: most people are not actively switching their bank, looking for a new payments tool, or thinking about investment products on any given day. Marketing that only activates at the moment of intent misses the vast majority of its future customers.

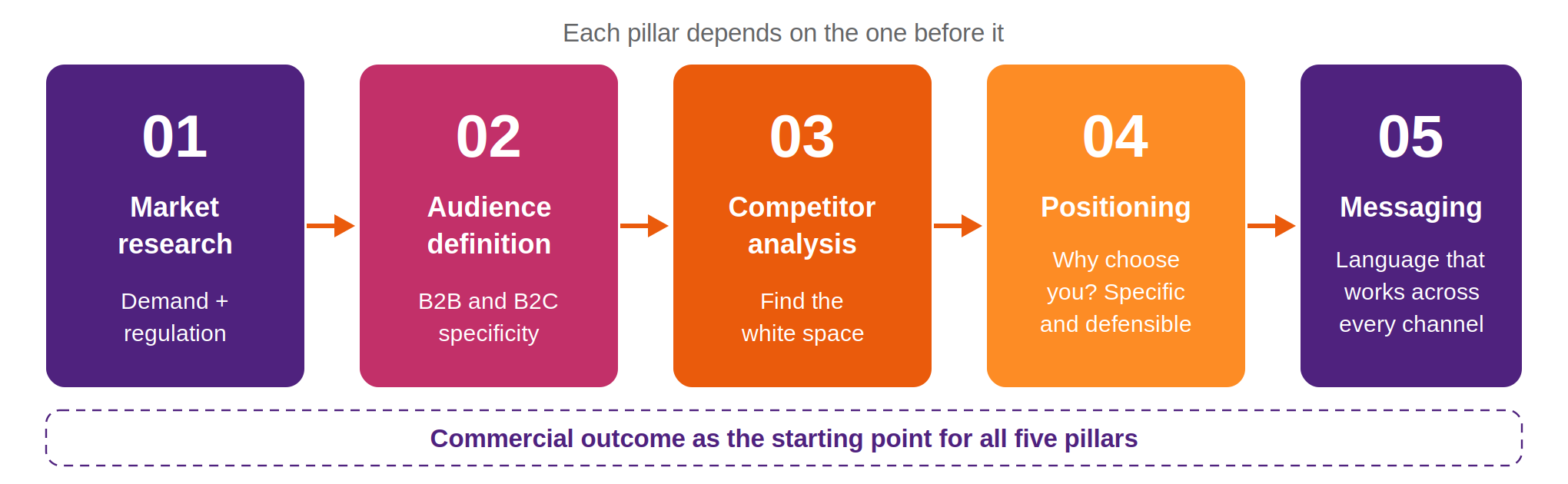

The 5 pillars of a fintech marketing strategy

1. Market research

Before anything else, you need to understand the market you're in.

That means understanding where demand is genuinely growing and where it's plateauing. It means understanding how the regulatory environment shapes your customers' decisions. For B2B fintech, the EU's Digital Operational Resilience Act, which came into full application in January 2025, has changed how financial institutions procure and evaluate technology vendors. For consumer fintech, FCA consumer duty obligations in the UK shape what you can claim, how you must communicate, and what fair outcomes look like in practice. Knowing the regulatory context isn't background reading. It's market intelligence.

It also means knowing who your competitors are actually targeting, where the gaps are, and which positions in the market are genuinely available to you. Market research in fintech needs to be ongoing. This is a sector that moves fast enough to make last year's assumptions a liability.

2. Audience definition

Most fintech companies have a broader idea of their audience than they need.

"UK adults" is not an audience. "26 to 40 year old professionals who are frustrated with their high-street bank and are comfortable managing money through their phone" is getting somewhere. "Mid-market European banks undergoing digital transformation with a CTO who owns the infrastructure decision" is more useful still. The principle is the same whether you're selling to a consumer or to an enterprise: specificity is what makes marketing work.

Forrester's 2026 State of Business Buying found that a typical B2B purchasing decision now involves 13 internal stakeholders and 9 external influencers, and for complex or AI-adjacent purchases, that buying group can double. In consumer fintech, the equivalent challenge is understanding the decision-making context: the triggers that shift someone from passive awareness to active consideration, and the moments where a competitor is most likely to intercept them first.

Vague audience definition produces vague marketing. The precision you apply here determines the precision of everything that follows.

3. Competitor analysis

Competitor analysis in fintech marketing isn't about copying what's working elsewhere. It's about finding the space your competitors haven't occupied, and working out whether that space is available for a reason or whether it's been overlooked.

That means looking at their messaging, their content, their channel mix, their customer reviews, and their product positioning. It means identifying the claims everyone in your category makes and working out which are meaningfully different from yours and which are just noise.

Peer review platforms deserve more attention than most fintech companies give them. G2's 2024 Buyer Behavior Report found that independent review sites are now the primary information source for 31% of B2B buyers, up from 13% in 2021. For consumer fintech, app store reviews and comparison sites play a similar role. Where your brand shows up and what it says in those spaces is part of your competitive positioning whether you've chosen to manage it or not.

4. Positioning

Your positioning is the answer to one question: why should someone choose you over every available alternative?

That question applies whether "someone" is a consumer who's seen five banking apps this week or a Head of Compliance at a regulated financial institution who's been asked to evaluate four vendors. Strong fintech positioning is specific, credible, and defensible. Not "we're trusted" or "we make finance simpler." A clear statement of who you serve, what problem you solve better than anyone else, and why, backed by evidence.

The trust dimension matters more in financial services than in almost any other sector. Edelman's 2025 Trust Barometer puts global financial services trust at 64%, the first time the industry crossed into "trusted" territory since 2008. That trust is hard-won and fragile. Positioning that overpromises erodes it fast, in both consumer and B2B markets.

Positioning work is uncomfortable because it forces choices. That's exactly why most fintech companies avoid it, and why the ones that do it properly tend to stand out.

5. Messaging

Once positioning is clear, messaging is the translation of that positioning into language that works across every channel and every audience segment.

In consumer fintech, that often means making something complex feel simple and safe, without being so simplified that it undersells the product. In B2B fintech, messaging has to land at two levels simultaneously: for the technical buyer who scrutinises every claim, and for the business buyer who cares primarily about commercial outcomes and risk.

Edelman and LinkedIn's 2024 B2B Thought Leadership Impact Report found that 73% of B2B decision-makers consider thought leadership more trustworthy than traditional marketing materials for assessing a company's capabilities. The consumer equivalent is social proof: reviews, case studies, and evidence of real outcomes. In both markets, demonstrating expertise is more persuasive than asserting it.

Fintech branding

Brand in fintech does more commercial work than most companies give it credit for.

In consumer fintech, brand is often the primary reason someone tries you in the first place, and the primary reason they stay. When the underlying product is functionally similar to a competitor's, the brand experience — how you communicate, what you stand for, how you make someone feel about their money — becomes the differentiator.

In B2B fintech, brand operates differently but matters just as much. 6sense's 2025 B2B Buyer Experience Report found that 95% of winning vendors were already on the buyer's shortlist before formal evaluation began. That shortlist is built almost entirely on brand familiarity, reputation, and what the buyer has absorbed about a company over time, long before any sales conversation. You can't win a deal from a shortlist you're not on. And you don't get on the shortlist without brand presence.

What fintech brand actually consists of

Brand in fintech is not just a logo and a colour palette. It's the accumulated impression your company leaves across every touchpoint — your website, your content, your ads, your customer support, your product interface, your presence at industry events, your coverage in the trade press.

A few things matter most in a fintech context:

Credibility signals. Regulatory references, security certifications, named clients, and verifiable results all contribute to whether someone trusts you enough to engage. In financial services, these aren't nice-to-haves. They're table stakes.

Clarity of proposition. Fintech markets are full of vague claims. "The future of finance" and "smarter banking for modern businesses" are not positions. They're noise. A brand that can say clearly and specifically what it does, for whom, and why that matters, will stand out against competitors who can't.

Consistency across channels. The impression your brand creates should be coherent whether someone encounters you on LinkedIn, through a Google search, in a trade publication, or on a referral from a peer. Inconsistency creates doubt, and doubt is expensive in a sector where trust is the purchase criterion.

Visual identity that earns attention. Financial services has historically defaulted to the conservative — blues, greens, white space, stock photography of handshakes. The fintech brands that break through tend to make different choices. They look like they belong in the world their customers live in, not the world their founders grew up in.

The fintech customer journey

Marketing strategy has to be built around how customers actually make decisions, not how we'd prefer them to.

In consumer fintech, the journey from first awareness to conversion can be short. Someone sees an ad, reads a few reviews, tries the app, decides within days. But retention is where most consumer fintech businesses win or lose, and the marketing that supports retention looks very different from the marketing that drives acquisition. Treating them as the same strategy, which many fintech companies do, is an expensive mistake.

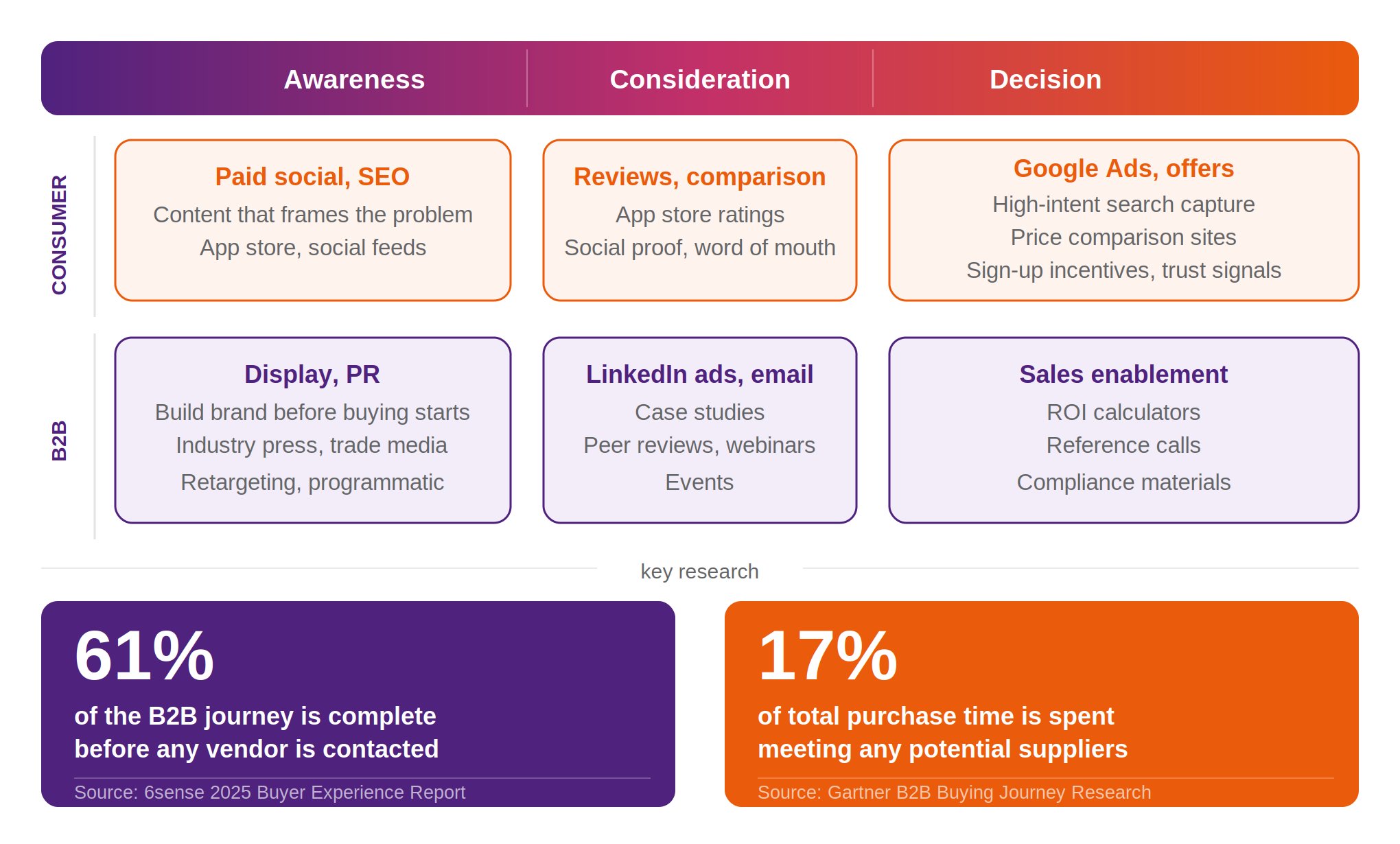

In B2B fintech, the timelines are longer and the process more formal. 6sense's 2025 B2B Buyer Experience Report, based on a sample of over 4,000 buyers, found that buyers now complete approximately 61% of their purchasing journey before first contacting a vendor. More telling: 95% of winning vendors were already on the buyer's shortlist on day one of their search. The vendor contacted first wins around 77 to 80% of deals. If your brand isn't in the consideration set before the buying process formally begins, your sales team is playing catch-up from the first call.

Both models share a common implication. Gartner research consistently finds that buyers spend only around 17% of their total purchase time meeting with potential suppliers, and far less than that with any single vendor. Most of the evaluation, in both consumer and B2B contexts, happens independently. Content, brand presence, organic search, and social proof do the majority of the work before any direct contact occurs.

Your strategy needs to work at each stage of that journey.

Awareness. The prospective customer or buyer knows they have a problem but hasn't defined a solution yet. Content that helps them frame their problem, and that frames it in a way that points naturally towards what you do, is the most valuable thing you can produce here.

Consideration. They're actively evaluating options. Reading comparison content, checking reviews, asking peers, watching demos. Demand Gen Report's research found that 62% of B2B buyers engage with three to seven pieces of content before connecting with sales. In consumer markets, the equivalent is the research phase before download or sign-up. Social proof and clear differentiation move people through this stage. Not more content. Better content.

Decision. They're choosing between a shortlisted set of options. For consumer fintech this is about what tips someone over the line: targeted offers, Google Ads capturing high-intent search, price comparison site presence, and trust signals that reduce the residual doubt before sign-up. For B2B, it's sales enablement, case studies, ROI calculators, and reference conversations.

Executing your fintech marketing strategy

Strategy sets the direction. Execution is where it either holds together or falls apart.

The five approaches below are not alternatives to each other. They serve different purposes at different stages of the customer journey, and the best fintech marketing programmes combine them deliberately rather than defaulting to whichever one the team is most comfortable with.

Fintech inbound marketing

Inbound marketing is about making your business findable to buyers and customers who are already looking.

The core components are organic search, content, and a website that converts traffic into pipeline or sign-ups. Done well, inbound compounds over time. A piece of content that ranks for a relevant query today can generate leads for years without further investment. HubSpot's research consistently shows inbound-generated leads cost around 61% less than outbound-sourced ones.

For B2B fintech, inbound tends to work best for mid-funnel queries, the searches buyers make when they're actively evaluating categories and solutions. "What is RegTech?" and "best embedded finance platforms for mid-market banks" are inbound opportunities. Someone already knows they have a problem and is researching how to solve it. Content that answers those questions well, and that connects them to your specific offering, is highly efficient pipeline generation.

For consumer fintech, inbound covers SEO for high-intent queries ("best savings account for freelancers"), comparison site presence, and app store optimisation. The same principle applies: be findable at the moment someone is actively looking, and make the case clearly when they find you.

The limitation of inbound on its own: it only reaches the people who are already searching. Given that only around 5% of B2B buyers are in-market at any time (Ehrenberg-Bass), and consumer fintech buyers are rarely in active switching mode, inbound alone will always leave the majority of your addressable market untouched.

Fintech demand generation

Demand generation is about creating buying intent in people who aren't yet looking.

The distinction from inbound is important. Inbound captures existing demand. Demand generation creates new demand. In practice this means paid media, programmatic display, sponsored content in industry publications, LinkedIn advertising, and outbound programmes, all designed to put your brand and proposition in front of people before they've started a buying process.

For B2B fintech, demand generation is particularly valuable in emerging categories where buyers don't yet know they have the problem your product solves. RegTech, embedded finance, and open banking infrastructure all require category education before product consideration. You can't capture demand that doesn't exist yet. You have to create it first.

The tradeoff is clear: demand generation produces faster results than inbound but requires consistent investment. When you stop spending, it stops working. The companies that get the balance right treat inbound as the long-term compound investment and demand generation as the accelerant that fills pipeline in the near term.

LinkedIn research with Nielsen found LinkedIn advertising to be 5x more effective than TV and display for financial services brands, and 4x more efficient than search at the consideration stage. For B2B fintech marketers with limited budgets choosing where to concentrate demand generation spend, that's a meaningful data point.

ABM in fintech

Account-Based Marketing treats specific companies as markets of one. Rather than casting a wide net and hoping the right people fall in, ABM identifies a finite list of target accounts and builds personalised, multi-touchpoint campaigns aimed directly at the buying committee within each of them.

It's particularly well-suited to B2B fintech for two reasons. The addressable market is often small enough that broad-reach marketing is inefficient. And deal values are typically large enough to justify the higher cost-per-engagement of account-level personalisation.

The results when ABM is done properly are material. Momentum ITSMA's 2024 Global ABM Benchmark found 81% of marketers report higher ROI from ABM than other marketing initiatives. Forrester found that organisations focused on buying groups, the core unit of ABM thinking, saw 17 times higher conversion rates compared to lead-centric approaches. Demandbase's 2026 State of ABM report found companies tracking three to four buying groups per account see 48.5% higher win rates than those that don't.

ABM works best when your ICP is tightly defined and your target account list is genuinely finite, when sales and marketing are aligned on which accounts to prioritise and what success looks like, and when you have the content infrastructure to support personalised campaigns across a full buying committee.

Done badly, which usually means running ABM tactics without ABM thinking, it's an expensive way to generate a list of names who never convert.

Fintech product marketing tactics

Product marketing sits at the intersection of the product, the market, and the commercial team. In fintech, it's one of the most underdeveloped marketing disciplines, and one of the most commercially important.

The job of product marketing in fintech is to translate what a product does into language that means something to the person who has to buy it. That sounds straightforward. It rarely is. The technical complexity of many fintech products, combined with the gap between how engineers describe them and how buyers think about their problems, creates a communication failure that loses deals and slows growth.

A few things that product marketing in fintech specifically requires:

Persona-specific positioning. The same product needs to be positioned differently for the technical evaluator, the economic buyer, and the compliance stakeholder. Each of them has different concerns. Each of them needs to hear a different answer to the question "why should we choose this?"

Competitive battlecards. In a crowded market, your sales team will regularly meet buyers who are evaluating you against two or three alternatives. Equipping them with clear, honest, and specific comparisons — rather than generic claims about being "best in class" — wins deals.

Case studies built around outcomes, not features. A prospect doesn't care that your API processes 10,000 transactions per second. They care that a bank like theirs used your product and reduced compliance costs by 30% in six months. The £3.2m pipeline we generated for KYC360 is a more persuasive piece of content than any feature list.

Launch planning that goes beyond announcements. Product launches in fintech are often treated as communications exercises — press releases, LinkedIn posts, email newsletters. The marketing opportunity is usually much larger: a well-timed launch can anchor a content campaign, drive inbound traffic for months, and give the sales team a reason to re-engage dormant prospects.

Fintech content marketing

Content marketing in fintech has a specific structural challenge. The people who most need to read your content, senior decision-makers at financial institutions or high-value consumer segments, are also the people with the least time and the highest bar for what they'll engage with

Generic, volume-led content strategies don't work here. The CMI 2025 B2B Content Marketing Benchmarks found that 87% of B2B marketers say content marketing helped create brand awareness, but 51% of B2B buyers said content they received in 2024 was too generic or irrelevant. The gap between production and impact is significant.

What works in fintech content marketing is different from what works in most B2B sectors.

Genuine expertise, not category education. Your audience already knows what RegTech is, or what open banking means, or why consumer trust matters. Content that explains the basics wastes their time. Content that offers a specific, defensible point of view on a topic they're actively grappling with earns their attention.

Original research and data. The 488% increase in blog traffic we delivered for Cambridge Global Payments was driven in large part by content built around data and proprietary insight. Content that cites original research attracts links, gets shared within buying committees, and positions the brand as a genuine source of intelligence rather than a vendor producing marketing materials.

Formats that match how buyers consume content. Long-form guides rank well and serve buyers at the research stage. Short, direct LinkedIn posts build brand familiarity with out-of-market buyers. Webinars and events create depth with prospects at consideration stage. The best fintech content programmes use all three rather than defaulting to one format.

Content for the whole buying committee. Most B2B fintech content is written for the person who's easiest to reach, which is usually someone in marketing or operations. The people who actually sign off the budget, the CFO, the CTO, the Head of Risk, consume different content in different places. A content strategy that doesn't reach them isn't a content strategy. It's a comfort activity.

Developing your fintech marketing plan

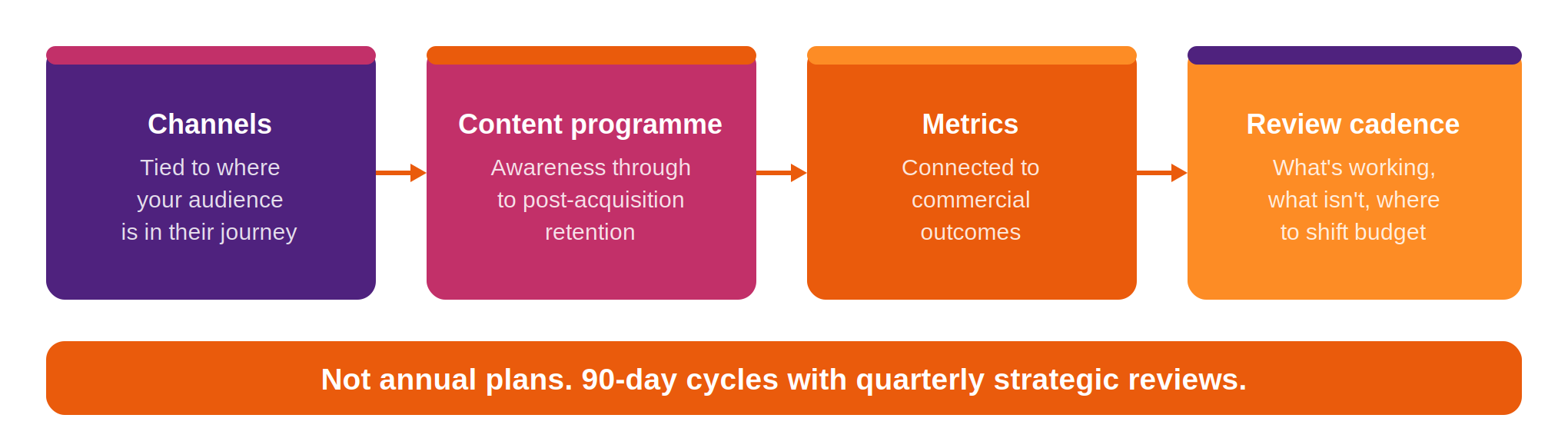

Once the strategic foundations are in place, audience definition, positioning, messaging, and journey mapping, the plan translates all of that into prioritised activity with timelines and budgets attached.

A good fintech marketing plan sets out the specific channels you're investing in and why, tied to where your audience is in their journey. It sets out the content programme that supports each stage, not just blog posts, but the materials that support conversion at consideration stage and retention after acquisition. It sets out the metrics that matter, the indicators that connect marketing activity to commercial outcomes. And it sets out the review cadence, how often you're looking at what's working and where budget should shift.

We don't believe in annual marketing plans. The market moves too quickly. The best fintech marketing programmes run on 90-day cycles with quarterly strategic reviews.

Working with a fintech marketing agency

Most fintech companies come to us after a period of marketing that produced activity but not results. They've been producing content nobody reads, running campaigns that generate clicks but not conversions, or struggling to explain to the board why the investment isn't moving the numbers that matter.

The common thread is almost always the same. The activity wasn't grounded in a clear strategy. It was built around a channel or a campaign, and when the campaign ended, so did the momentum.

Every engagement at Curious Cat Digital starts with the commercial question: what does the business need marketing to deliver, and by when? Then we work backwards from that through the funnel, or the customer journey, or whatever shape the market actually takes for that business.

What would the next six months look like if you worked with a Fintech Marketing Agency